Payment boom without cash

In recent years, Vietnam has seen an explosion of cashless payment methods, including credit cards, Internet Banking, e-wallets and other digital payment applications. Vietnamese consumers are increasingly actively accepting digital payments because of the convenience and speed of payment, so this payment method is used more frequently in direct door-to-door transactions. goods and online shopping.

Meanwhile, the Government of Vietnam also aims to reduce cash transaction rate from 90% in 2016 to 10% by the end of 2020. About two-thirds of Vietnam’s population is using the Internet and 72% of the population is use smart phones in 2018. Vietnam e-commerce has recorded an impressive growth of 25-30% in recent years, thanks to the growing middle class and likes shopping. These facts prove that Vietnam is a potential market for cashless payment services.

According to market research company Statista, the total value of transactions using digital payment solutions in Vietnam will reach 8.52 billion USD in 2019. The growth rate of this field in the period of 2019-2023 is estimated. an average of 12.7% / year, equivalent to the total value of transactions using digital payment solutions to reach 13.74 billion USD in 2023.

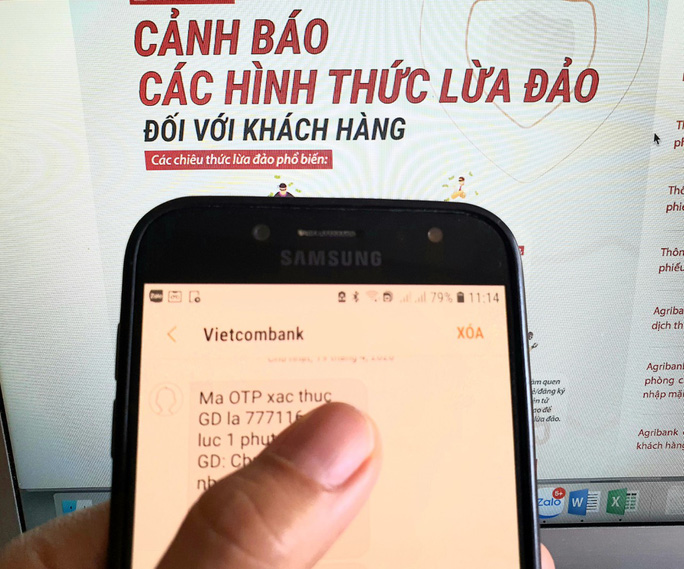

However, the increasing number of cashless transactions is also the main reason leading to the increasing demand for payment security. According to a survey on consumer payment behavior conducted by Visa, security is still a top concern of Vietnamese consumers when using non-cash payment.

Specifically, when asked about the most worries about using a phone to pay, Vietnamese consumers listed cases such as when they lost their phone, hacked phone or unauthorized access to their personal data. kernel, phone infection, or malware installation.

In order to tighten payment security towards a cashless future, Visa – the world’s leading payment technology company – announced the Payment Security Roadmap for Vietnam in March 2019. Visa’s roadmap focuses on exploiting groundbreaking initiatives, supporting the development of payment security, in order to meet the speed at which technology is changing the payment behavior of consumers.

The year of payment security predictions needs to be noted in the new decade

To date, the digital payment industry has made significant progress in assessing the level of risk, preventing fraud, protecting billions of transactions in the form of new payments made by users. Entering a new decade, the continued expansion of digital payments in Vietnam and around the world will present opportunities and challenges. Visa has released 5 payment security predictions to keep in mind over the new decade.

The world will witness a strong growth in the adoption of payment tokens and in particular Chip EMV 3D Secure technology.

As the challenges of payment fraud continue, digital identities may end up using passwords. Therefore, consumers can switch to more secure authentication methods such as face, fingerprint or voice authentication. European consumers will begin to experience Strong Customer Authentication (SCA). This is the European Union’s request for consumers for multi-layer verification when making digital transactions. As financial institutions and businesses meet these requirements in Europe, global companies can find ways to expand the most innovative authentication solutions to other markets.

Businesses and financial institutions will have to meet customers’ high-speed payment needs with new, fast and secure forms of payment. Currently, Visa is working on more innovative payment methods, from biometric authentication and wearables to new mobile applications such as digital issue cards at the Tokyo Olympic Games and Paralympics. 2020.

Real-time payment (RTP) is another global initiative that has flourished in recent years. However, this payment method will require a new approach to prevent fraud. It is worth noting that many businesses also expect the speed and convenience of payment methods, so wire transfer via banks and check payments are gradually replaced by form of instant payment (instant payment). However, speed and convenience are not synonymous with payment security.

As the volume of payments between RTP networks and peer-to-peer (P2P) networks grows, there will be many identifiable and unrecognizable vulnerabilities in systems that need to be quickly addressed. Therefore, RTP suppliers and financial institutions need to improve handling and strengthen cooperation with trusted partners in payment security to address this challenge.

In addition, the increasing use of artificial intelligence (AI) will continue to promote new products and services in payment, having a significant impact on society. However, AI also has challenges when used by bad objects. For example, the Internet has split to become a floating, black and sunken website, or a social network being used beyond its original purpose of connecting friends and family. The challenge of applying AI in the coming years requires joint efforts of industries to limit the downside of technology and ensure that AI is used to bring about opportunities and social progress.

Above all, users will continue to be the weakest link in the digital process. Technology has been trying to solve this problem for a long time – from spell checking in word processors and email applications, to automatic braking in some cars today. Advances in payment security, such as Chip EMV technology, will help reduce payment fraud. However, technology can only prevent fraud to a certain extent, because it still needs to be operated by people and people often make mistakes.

In addition, non-technical (social engineering) attacks will continue to evolve, targeting non-alert users. As long as one person becomes a victim, the entire organization or network will be at risk. Therefore, financial institutions, banks need to universalize and give users the essential tools, because they are the “first line of defense” and important.

People, businesses and organizations will grow when barriers are removed and confidence is strengthened. Keeping that belief requires innovation, making choices, as well as increasing the commitment to payment security. This is the best time for us to lead and accelerate the change in payment security and create a catalyst for growth. By drawing lessons from the past few years, we can both tackle future challenges and take advantage of opportunities in today’s increasingly digital society.

Paul Fabara (General Manager of Visa Risk Management)

Tin tức khác

The first Vietnamese bank allowing customers to use domestic cards for transactions in Korea

In addition to international debit cards or credit cards, TPBank has allowed all domestic cardholders to make instant payment and withdrawal transactions in the Korean market. Tien Phong Commercial Joint Stock Bank (TPBank) has successfully implemented the project of 3-party connection between TPBank, Vietnam National Payment Joint Stock Company (NAPAS) and BC Card Company –

More

Why you need to use an ATM chip card ?

Increasing safety, high information security, minimizing the risk of fraud, stealing card information (skimming) … are the outstanding advantages that chip technology cards bring. Recently, banks have been offering ATM cards based on domestic VCCS card standards, complying with EMV international standards as well as increasing communication to their customers about this conversion. Why should

More

Converting magnetic card to chip card: Increasing security and safety when using the card

Under the direction of the State Bank, Vietnam Bank Card Association (VBCA) in collaboration with Vietnam National Payment Corporation (NAPAS) officially launched domestic chip card products. The Securities Investment Newspaper had an interview with Mr. Tran Cong Quynh Lan, Deputy General Director of VietinBank, one of the first 7 banks to deploy this event. Switch

More

Add a bank alert trick trick to steal money in the account

Although banks have repeatedly warned of high-tech criminals cheating on OTP codes, requiring login to fake bank websites to steal customers’ money, there are still many people trapped. Agribank has continued to warn tricks of branding, website, relatives, bank officials, postal staff, law enforcement agencies … with many scenarios to steal customers’ account information. ,

More

From 2020, does the social insurance book no longer exist?

The social insurance book has been familiar to employees for a long time, is a book that records the employees’ participation in social insurance and is also a “proof” for them to enjoy all the prescribed regimes. specified. However, it is possible that this book will no longer exist. One of the important changes in

More

Xử phạt vi phạm luật giao thông: Đề xuất nộp phạt qua thẻ chip ngân hàng

Việc xử phạm vi phạm an toàn giao thông thông qua thẻ chip ngân hàng là cần thiết, phù hợp với xu thế chung… Mỗi năm có hàng triệu trường hợp vi phạm hành chính trong lĩnh vực giao thông, với số tiền phạt lên đến hàng ngàn tỷ đồng. Riêng 9 tháng năm 2019,

More